EViews 9.5 New Features

EViews 9.5 New Econometrics and Statistics: Forecasting

EViews features a number of additions and improvements to its toolbox of basic statistical procedures. Among the highlights are new tools for automatic ARIMA forecasting, forecasting evaluation and averaging, and VAR forecasting.

Automatic ARIMA Forecasting

Automatic ARIMA forecasting is a method of forecasting values for a single series based upon an ARIMA model.

Although EViews provides sophisticated tools for estimating and working with ARIMA models using the familiar equation object, there is considerable value in a quick-and-easy tool for performing this type of forecasting. EViews introduces an automatic ARIMA forecasting series procedure that allows the user to quickly determine an appropriate ARIMAX specification and use it to forecast the series into the future.

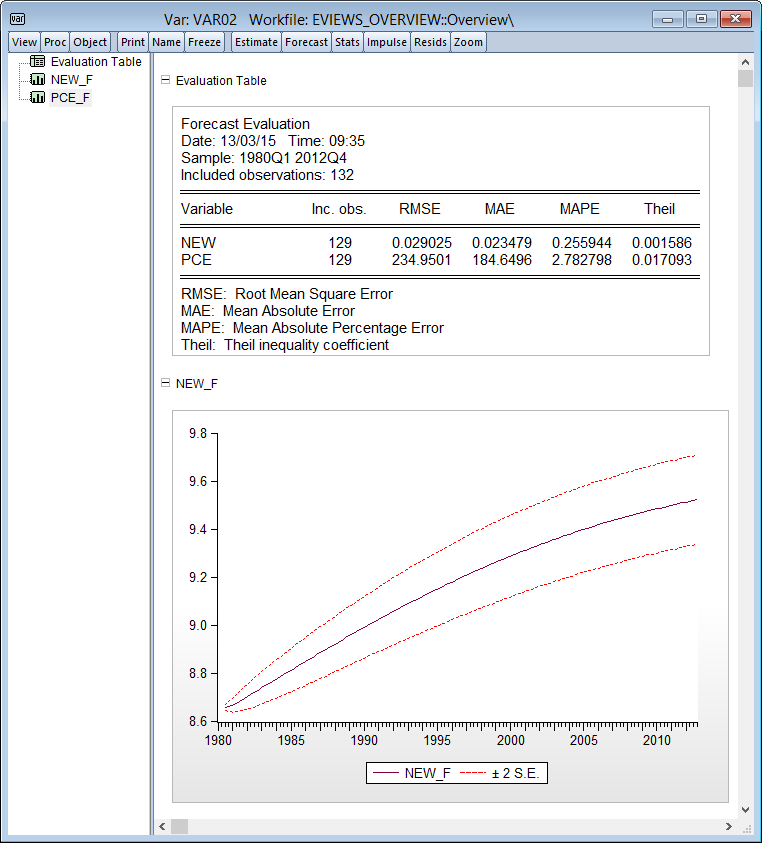

Forecast Evaluation

EViews provides tools for evaluating the quality of a forecast which can help you determine which single forecast to use, or whether constructing a composite forecast by averaging would be more appropriate.

When constructing a forecast of future values of a variable, economic decision makers often have access to different forecasts; perhaps from different models they have created themselves or from forecasts obtained from external sources. When faced with competing forecasts of a single variable, it can be difficult to decide which single or composite forecast is "best", EViews 9 provides tools to solve for these problems.

EViews computes four different measures of forecast accuracy:

- RMSE (Root Mean Squared Error)

- MAE (Mean Absolute Error)

- MAPE (Mean Absolute Percentage Error)

- Theil Inequality Coefficient

In addition, EViews can compute the Combination Test, or Forecast Encompassing Test (Chong and Hendry, 1986; Timmermann, 2006) for evaluating whether averages of forecasts perform better than the individual forecasts.

The Forecast Evaluation Series View has been extended with the addition of the Diebold-Mariano test as part of the output whenever two forecasts are being evaluated.

The Diebold-Mariano test allows for statistical comparison of the accuracy of two competing forecasts of the same data.

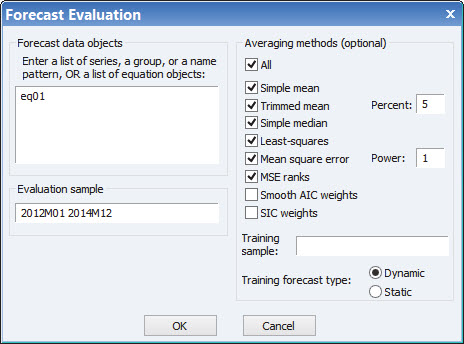

Forecast Averaging

EViews offers a number of easy-to-use tools for performing forecast averaging using simple mean, least squares, mean square error, mean square error ranks, smoothed AIC, approximate Bayesian model averaging trimmed mean and simple median methods.

A number of studies (Timmermann 2006) have shown that averaging forecasts is more accurate than choosing a single best forecast. Forecast averaging, or forecast combining, is a methodology for combining multiple forecasts into a single forecast, which is often a superior method to picking which single forecast was “best” out of the individual forecasts available.

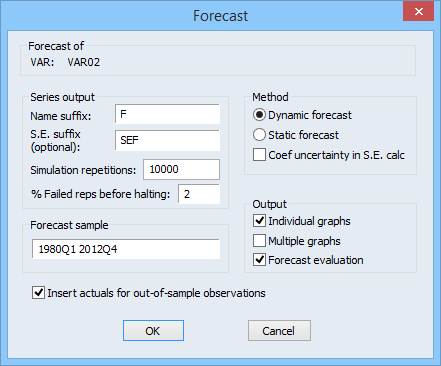

VAR Forecasting

Now you can produce forecasts directly from an estimated VAR object by updating the Forecast dialog box. This now eliminates the need to first make an EViews model object from the VAR and then solve the model.