Name | Function | Description |

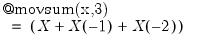

@movsum(x,n) | n-period backward moving sum |  . NAs are propagated. . NAs are propagated. |

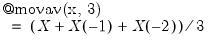

@movav(x,n) | n-period backward moving average |  NAs are propagated. NAs are propagated. |

@movavc(x,n) | n-period centered moving average | centered moving average of X. Note if n is even then the window length is increased by one and the two endpoints are weighted by 0.5. NAs are propagated. |

@movstdev(x,n) | n-period backwards moving standard deviation | sample standard deviation (division by  ) of X for the current and previous ) of X for the current and previous  observations. NAs are propagated. observations. NAs are propagated. |

@movstdevs(x,n) | n-period backwards moving sample standard deviation | sample standard deviation (division by  ) of X for the current and previous ) of X for the current and previous  observations. Note this is the same calculation as @movstdev. NAs are propagated. observations. Note this is the same calculation as @movstdev. NAs are propagated. |

@movstdevp(x,n) | n-period backwards moving population standard deviation | population standard deviation (division by  ) of X for the current and previous ) of X for the current and previous  observations. NAs are propagated. observations. NAs are propagated. |

@movvar(x,n) | n-period backwards moving variance | population variance (division by  ) of X for the for the current and previous ) of X for the for the current and previous  observations. NAs are propagated. observations. NAs are propagated. |

@movvars(x,n) | n-period backwards moving sample variance | sample variance (division by  ) of X for the current and previous ) of X for the current and previous  observations. NAs are propagated. observations. NAs are propagated. |

@movvarp(x,n) | n-period backwards moving population variance | population variance (division by  ).of X for the current and previous ).of X for the current and previous  observations. Note this is the same calculation as @movvar. NAs are propagated. observations. Note this is the same calculation as @movvar. NAs are propagated. |

@movcov(x,y,n) | n-period backwards moving covariance | population covariance (division by  ) between X and Y of the current and previous ) between X and Y of the current and previous  observations. NAs are propagated. observations. NAs are propagated. |

@movcovs(x,y,n) | n-period backwards moving sample covariance | sample covariance (division by  ) between X and Y of the current and previous ) between X and Y of the current and previous  observations. NAs are propagated. observations. NAs are propagated. |

@movcovp(x,y,n) | n-period backwards moving population covariance | population covariance (division by  ) between X and Y of the current and previous ) between X and Y of the current and previous  observations. Note this is the same calculation as @movcov. NAs are propagated. observations. Note this is the same calculation as @movcov. NAs are propagated. |

@movcor(x,y,n) | n-period backwards moving correlation | correlation between X and Y of the current and previous  observations. NAs are propagated. NAs are propagated. observations. NAs are propagated. NAs are propagated. |

@movmax(x,n) | n-period backwards moving maximum | the maximum of X for the current and previous  observations. NAs are propagated. observations. NAs are propagated. |

@movmin(x,n) | n-period backwards moving minimum | the minimum of X for the current and previous  observations. NAs are propagated. observations. NAs are propagated. |

@movsumsq(x,n) | n-period backwards sum-of-squares | the sum-of-squares of X for the current and previous  observations. NAs are propagated. observations. NAs are propagated. |

@movskew(x,n) | n-period backwards skewness | the skewness of X for the current and previous  observations. NAs are propagated. observations. NAs are propagated. |

@movkurt(x,n) | n-period backwards kurtosis | the kurtosis of X for the current and previous  observations. NAs are propagated. observations. NAs are propagated. |

@movobs(x,n) | n-period backwards nmber of non-NA observations | the number of non-missing observations in X for the current and previous  observations. Note this function always returns the same value as @mobs. observations. Note this function always returns the same value as @mobs. |

@movnas(x,n) | n-period backwards nmber of NA observations | the number of missing observations in X for the current and previous n-1 observations. Note this function always returns the same value as @mnas. |

@movinner(x,y,n) | n-period backwards inner product of X and Y | inner product of X and Y for the current and previous  observations. NAs are propagated. observations. NAs are propagated. |

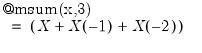

@msum(x,n) | n-period backward moving sum |  NAs are not propagated. NAs are not propagated. |

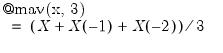

@mav(x,n) | n-period backward moving average |  NAs are not propagated. NAs are not propagated. |

@mavc(x,n) | n-period centered moving average | centered moving average of X. Note if n is even then the window length is increased by one and the two endpoints are weighted by 0.5. NAs are not propagated. |

@mstdev(x,n) | n-period backwards moving standard deviation | sample standard deviation (division by  ) of X for the current and previous ) of X for the current and previous  observations. NAs are not propagated. observations. NAs are not propagated. |

@mstdevs(x,n) | n-period backwards moving sample standard deviation | sample standard deviation (division by  ) of X for the current and previous ) of X for the current and previous  observations. Note this is the same calculation as @movstdev. NAs are not propagated. observations. Note this is the same calculation as @movstdev. NAs are not propagated. |

@mstdevp(x,n) | n-period backwards moving population standard deviation | population standard deviation (division by  ) of X for the current and previous ) of X for the current and previous  observations. NAs are not propagated. observations. NAs are not propagated. |

@mvar(x,n) | n-period backwards moving variance | population variance (division by  ) of X for the for the current and previous ) of X for the for the current and previous  observations. NAs are not propagated. observations. NAs are not propagated. |

@mvars(x,n) | n-period backwards moving sample variance | sample variance (division by  ) of X for the current and previous ) of X for the current and previous  observations. NAs are not propagated. observations. NAs are not propagated. |

@mvarp(x,n) | n-period backwards moving population variance | population variance (division by  ) of X for the current and previous ) of X for the current and previous  observations. Note this is the same calculation as @movvar. NAs are not propagated. observations. Note this is the same calculation as @movvar. NAs are not propagated. |

@mcov(x,y,n) | n-period backwards moving covariance | population covariance (division by  ) between X and Y of the current and previous ) between X and Y of the current and previous  observations. NAs are not propagated. observations. NAs are not propagated. |

@mcovs(x,y,n) | n-period backwards moving sample covariance | sample covariance (division by  ) between X and Y of the current and previous ) between X and Y of the current and previous  observations. NAs are not propagated. observations. NAs are not propagated. |

@mcovp(x,y,n) | n-period backwards moving population covariance | population covariance (division by  ) between X and Y of the current and previous ) between X and Y of the current and previous  observations. Note this is the same calculation as @movcov. NAs are not propagated. observations. Note this is the same calculation as @movcov. NAs are not propagated. |

@mcor(x,y,n) | n-period backwards moving correlation | correlation between X and Y of the current and previous  observations. NAs are not propagated. observations. NAs are not propagated. |

@mmax(x,n) | n-period backwards moving maximum | the maximum of X for the current and previous  observations. NAs are not propagated. observations. NAs are not propagated. |

@mmedian(x,n) | n-period backward moving median | the median of X for the current and previous  observations. NAs are not propagated. observations. NAs are not propagated. |

@mmin(x,n) | n-period backwards moving minimum | the minimum of X for the current and previous  observations. NAs are not propagated. observations. NAs are not propagated. |

@msumsq(x,n) | n-period backwards sum-of-squares | the sum-of-squares of X for the current and previous  observations. NAs are not propagated. observations. NAs are not propagated. |

@mskew(x,n) | n-period backwards skewness | the skewness of X for the current and previous  observations. NAs are not propagated. observations. NAs are not propagated. |

@mkurt(x,n) | n-period backwards kurtosis | the kurtosis of X for the current and previous  observations. NAs are not propagated. observations. NAs are not propagated. |

@mobs(x,n) | n-period backwards number of non-NA observations | the number of non-missing observations in X for the current and previous  observations. Note this function always returns the same value as @movobs. observations. Note this function always returns the same value as @movobs. |

@mnas(x,n) | n-period backwards number of NA observations | the number of missing observations in X for the current and previous  observations. Note this function always returns the same value as @movnas. observations. Note this function always returns the same value as @movnas. |

@minner(x,y,n) | n-period backwards inner product of X and Y | inner product of X and Y for the current and previous  observations. NAs are not propagated. observations. NAs are not propagated. |