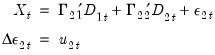

We will work with the standard triangular representation of a regression specification and assume the existence of a single cointegrating vector (Hansen 1992b, Phillips and Hansen 1990). Consider the  dimensional time series vector process

dimensional time series vector process  , with cointegrating equation

, with cointegrating equation

dimensional time series vector process , with cointegrating equation

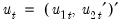

are deterministic trend regressors and the

are deterministic trend regressors and the  stochastic regressors

stochastic regressors  are governed by the system of equations:

are governed by the system of equations:

-vector of

-vector of  regressors enter into both the cointegrating equation and the regressors equations, while the

regressors enter into both the cointegrating equation and the regressors equations, while the  -vector of

-vector of  are deterministic trend regressors which are included in the regressors equations but excluded from the cointegrating equation (if a non-trending regressor such as the constant is present, it is assumed to be an element of

are deterministic trend regressors which are included in the regressors equations but excluded from the cointegrating equation (if a non-trending regressor such as the constant is present, it is assumed to be an element of  so it is not in

so it is not in  ).

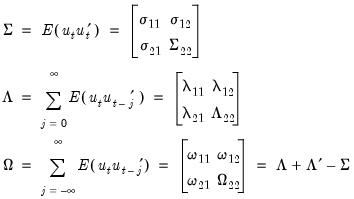

).  are strictly stationary and ergodic with zero mean, contemporaneous covariance matrix

are strictly stationary and ergodic with zero mean, contemporaneous covariance matrix  , one-sided long-run covariance matrix

, one-sided long-run covariance matrix  , and covariance matrix

, and covariance matrix  , each of which we partition conformably with

, each of which we partition conformably with

long-run covariance matrix

long-run covariance matrix  with non-singular sub-matrix

with non-singular sub-matrix  . Taken together, the assumptions imply that the elements of

. Taken together, the assumptions imply that the elements of  and

and  are I(1) and cointegrated but exclude both cointegration amongst the elements of

are I(1) and cointegrated but exclude both cointegration amongst the elements of  and multicointegration. Discussions of additional and in some cases alternate assumptions for this specification are provided by Phillips and Hansen (1990), Hansen (1992b), and Park (1992).

and multicointegration. Discussions of additional and in some cases alternate assumptions for this specification are provided by Phillips and Hansen (1990), Hansen (1992b), and Park (1992). in

in

, and cross-correlation between the cointegrating equation errors and the regressors

, and cross-correlation between the cointegrating equation errors and the regressors  . In the special case where the

. In the special case where the  are strictly exogenous regressors so that

are strictly exogenous regressors so that  and

and  , the bias, asymmetry, and dependence on non-scalar nuisance parameters vanish, and the SOLS estimator has a fully efficient asymptotic Gaussian mixture distribution which permits standard Wald testing using conventional limiting

, the bias, asymmetry, and dependence on non-scalar nuisance parameters vanish, and the SOLS estimator has a fully efficient asymptotic Gaussian mixture distribution which permits standard Wald testing using conventional limiting  -distributions.

-distributions. is no less than the number of stochastic regressors

is no less than the number of stochastic regressors  . Let

. Let  represent the number of cointegrating regressors less the number of deterministic trend regressors excluded from the cointegrating equation. Then, roughly speaking, when

represent the number of cointegrating regressors less the number of deterministic trend regressors excluded from the cointegrating equation. Then, roughly speaking, when  , the deterministic trends in the regressors asymptotically dominate the stochastic trend components in the cointegrating equation.

, the deterministic trends in the regressors asymptotically dominate the stochastic trend components in the cointegrating equation. case.

case.