EViews 13 New Features

EViews 13 New Econometrics and Statistics: Estimation

EViews 13 includes a number of new estimation techniques:

- Non-linear ARDL Estimation

- Improved PMG Estimation

- Difference-in-Difference Estimation

- Improved VEC Estimation

- Bayesian Time-varying Coefficient Vector Autoregression

Non-linear ARDL Estimation

EViews 13 offers improvements to existing tools for analyzing data using Autoregressive Distributed Lag Models (ARDL), featuring estimation of Nonlinear ARDL (NARDL) models which allow for more complex dynamics, with explanatory variables having differing effects for positive and negative deviations from base values.

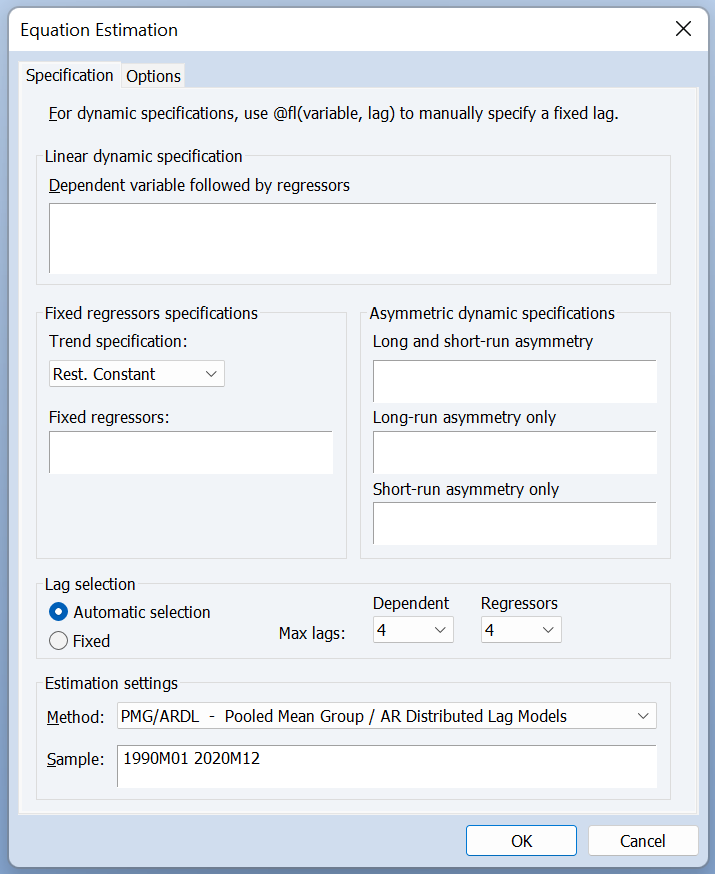

Improved PMG Estimation

EViews 13 extends the estimation of PMG models to support:

- A greater range of deterministic trend specifications (including those with fully restricted constant and trend terms)

- Specifications with asymmetric regressors.

Difference-in-Difference Estimation

Difference-in-difference (DiD) estimation is a popular method of causal inference that allows estimation of the average impact of a treatment on individuals.

EViews 13 offers tools for estimation of the DiD model using the common two-way fixed- effects (TWFE) method, as well as post-estimation diagnostics of the TWFE model, such as those by Goodman-Bacon (2021), Callaway and Sant’Anna (2021), and Borusyak, Jaravel, and Spiess (2021).

Improved VEC Estimation

Estimation of Vector Error Correction (VEC) models using reduced rank regression (RRR) has been a staple of EViews for several versions. Previous versions of EViews supported a variety of built-in specifications for deterministic trends, and allowed users to add unre- stricted exogenous regressors to account for short-term dynamics.

One important limitation of the existing tools for VEC estimation was the inability of users to add arbitrary exogenous variables to the cointegrating relation since the set of admissible restricted regressors was limited to the endogenous variables and potentially an intercept, and possibly a linear trend term.

EViews 13 removes this limitation on restricted regressors and improves on the prior treat- ment of exogenous variables in two distinct ways:

- By providing new deterministic trend assumption presets which allow for more flex- ible specification of restricted and unrestricted deterministic coefficients.

- By allowing users to add exogenous variables that are restricted to the cointegrating relation, variables that are unrestricted, and variables that in both the short and long-run equations, with an orthogonality assumption used to obtain the different coefficients.

Bayesian Time-Varying Coefficient VAR Estimation

Standard VAR models impose the constraint that the coefficients are constant through time. This is often not true of macroeconomic relationships. Consequently in recent years VAR estimators that allow coefficients to change have become popular.

Consequently, EViews 11 introduced Switching VAR - a class of VAR that allows discrete occasional changes in the coefficients of the VAR.

EViews 13 expands this further by introducing Bayesian Time-varying coefficient VAR models, which allow continuous smooth changes in the coefficients.